Green mortgages are not widely available, and not widely understood.

Just who exactly would need this type of mortgage and will the mortgage repayments be any cheaper than a normal mortgage?

The premise of a green mortgage is that it rewards the owners of only the most energy efficient properties, usually by offering a specially reduced interest rate. So there is a financial incentive to seek out these little known mortgage products.

Even though the UK mortgage market is the most competitive in the world, the grass is not always greener with a green mortgage. 😉

We take a look at what they are, what they offer and how to apply for one.

Table of Contents

- What is a green mortgage?

- Why do we need green mortgages?

- Which homes will qualify?

- What is an EPC rating?

- How do green mortgages work?

- Are green mortgages cheaper?

- Which lenders offer green mortgages?

- Qualifying for a green mortgage

- Is a green mortgage worth it?

- What are the pros and cons?

- Find an energy certificate online

- How do you apply?

- What’s in it for the lenders?

- Talk to an expert

What is a green mortgage?

A green mortgage rewards the owners of the most energy efficient properties with financial incentives.

This could be an existing property that you are about to buy, a new-build purchase or your current home that you have invested in to improve its eco credentials.

There’s no universal definition of what a green mortgage is, but currently it refers to the greenness (is that a real word?) of the property, rather than anything to do with the lender. Properties need to be officially graded as energy efficient to be eligible for these loans.

At the moment qualifying mortgages will usually be offered with lower interest rates than a regular mortgage from the same lender.

Why do we need green mortgages?

The UK as a whole is on a journey to become more energy efficient and reduce carbon emissions.

There are approximately 28 million households in the UK, comprising of all different types of houses and flats. When compared to other countries we have a lot more older properties, which are less efficient than the modern equivalents.

So the Government wants homeowners and landlords to make their properties greener, to reduce energy consumption and help to limit global warming.

Green mortgages are a way that borrowers can benefit from being more efficient as they have incentives that only apply to qualifying properties. They can also free up capital for home energy efficiency improvements via a capital raising remortgage.

Which homes will qualify?

Only the more energy efficient homes will qualify for a green mortgage.

To allow them to check which properties are the most efficient, lenders use the grading given on the most recent EPC. Only those rated A or B (in the top 20%) will qualify.

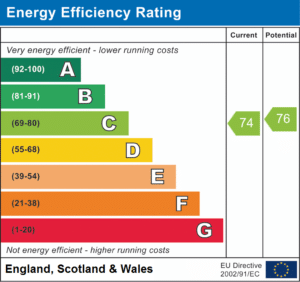

What is an EPC rating?

Your homes EPC rating is shown on it’s Energy Performance Certificate.

Every property needs an EPC when it is built and marketed for sale or rent. New-builds will have a Predicted Energy Assessment (PEA) which gives an estimated rating for off-plan or in-progress builds.

The EPC rating scores the energy efficiency of a property and also makes suggestions on how this could be improved. Ratings range from A (Best) to G (Worst).

A green mortgage lender will require a rating of either A or B.

Read more: Guide to EPCs

How to improve your rating

Switch to LED bulbs

Upgrade your boiler

Add solar panels

Improve the insulation

Install double glazing

How do green mortgages work?

These mortgages are only granted against properties that have an A or B rating from their EPC report.

MORTGAGE OPTIONS

The usual mortgage options are available, such as fixed rate, tracker or variable. You will also have a choice of repayment methods and repayment term.

AFFORDABILITY

As part of the underwriting process, a lender makes standard assumptions about the amount of money you spend on energy. These costs will be based upon averages.

However, a green mortgage lender recognises that a B rated property is cheaper to heat when compared to a G rated property. For their affordability calculations, this reduces your predicted monthly expenditure and allows you to take out a slightly bigger mortgage.

Are eco mortgages and green mortgages the same thing?

Not quite. An eco mortgage would be suitable for a home built in an environmentally friendly way, using sustainable materials. This is a very specific type of construction, with only a small number of active lenders.

A green mortgage tends to be aimed at properties that are more energy efficient, according to the EPC rating guide.

Are green mortgages cheaper?

Not always. Lenders will often provide cheaper deals, within their own product range, for more favourable EPC ratings. But a standard remortgage product from the wider mortgage market could be cheaper still. (just ask your broker to check)

Borrowing extra to make your home more energy efficient can often attract competitive rates from the green mortgage lenders, and will result in lower energy bills for you.

Which lenders offer green mortgages?

Even though the concept of a green mortgage has been around for over five years, there’s still only a small number of lenders offering them.

We do expect more lenders to adopt policies relating to the EPC grades, giving borrowers more choice.

Incentives tend to come in the form of a cheaper interest rate, or rate reduction, or a cashback.

It’s not always clear how you can qualify for these deals, so we would suggest speaking with a mortgage broker who can search the market for the most suitable.

Barclays

Halifax

Nationwide BS

NatWest

TSB

Virgin Money

Kensington

Monmouthshire BS

Saffron BS

Qualifying for a green mortgage

This can be broken down into two parts:

The mortgage part

Here the usual loan to value and affordability aspects need to be satisfactory. Lenders will need to look at your credit report, request proof of income and establish your spending patterns.

The GREEN part

The criteria for the ‘green’ part will come from the energy performance certificate (EPC) for your property. You will be given an energy efficiency rating between A and G. With A being the best (most energy-efficient), and G being the worst.

You should be able to access a green mortgage if the rating is B or above. Some lenders specify an actual Standard Assessment Procedure (SAP) score, rather than a band. This is also shown on the EPC.

Standard Assessment Procedure (SAP) scores

- A = 92-100

- B = 81-91

- C = 69-80

- D = 55-68

Is a green mortgage worth it?

It’s important to properly compare your mortgage options, including green alternatives, before making a final decision. Don’t choose a mortgage on the basis that it is ‘green’, make sure it’s right for you and cost effective.

Green mortgages are an incentive for borrowers to buy more energy efficient homes, or to improve existing properties. This will then lead to lower energy bills. Homes that have a good EPC rating are often more expensive to buy and will hold their value better.

Lenders offering these schemes can help to reduce the UK’s domestic emission levels by encouraging homeowners to favour properties that are better insulated and more energy efficient. The reduction in the mortgage interest rate may be quite small but you will make savings in other areas by choosing to have a greener home.

What are the pros and cons?

Choosing to apply for a green mortgage would seem the sensible thing to do. If your property has an EPC rating of A or B then you qualify for these special rates. Let’s go ahead and get the paperwork done!

But wait just one minute.

Is it that clearcut? Are green mortgages always the best choice?

Let’s take a look at the advantages and disadvantages.

You could benefit from a discounted interest rate

You could benefit from a cashback payment

They can be a good incentive to make your home more energy efficient

You might be able to borrow more money as your energy costs will be lower

It makes you feel good

Most people will be able to find a standard mortgage that is cheaper

Not everyone can qualify

The actual mortgage is not ‘green’

The availability is limited to a small number of lenders

It’s expensive to improve the EPC rating

Find an energy certificate online

Energy performance certificates need to be registered on a government website.

You can search to view a certificate by postcode, street name and town, or certificate number.

How do you apply?

Applying for a green mortgage is not so different to applying for a regular mortgage.

But first you need to find a lender that caters for these mortgage types. All of the current providers need your property to have either an A or B rating from the EPC. They will need to verify this along with your income, credit history, mortgage deposit etc.

You can check your EPC here: https://www.gov.uk/find-energy-certificate

If your loan to value and earnings are enough for the mortgage you need, then it’s time to apply. All of the usual documents will be required:

- Proof of ID

- Proof of income

- Proof of earnings

- Bank statements

- Proof of deposit

Before you grab a pen there’s just one more task.

Speak to an independent mortgage broker so you can compare your green mortgage to the best from all of the other lenders. Remember, there’s nothing ‘green’ about the mortgage itself, this only relates to your property.

In many cases a more competitive deal can be found elsewhere.

It’s still early days for these types of mortgage, and no doubt many more lenders will offer them over the coming years. But for now, the best deals can be found by a qualified mortgage broker.

What’s in it for the lenders?

Energy efficiency is all well and good, but lenders operate to make money, so what’s in it for them?

There is some evidence that green buildings, along with their owners, are less likely to pose a lending risk for the banks.

We know that greener homes cost less to heat. So with lower utility bills, your monthly affordability improves.

For some years now the UK government has been encouraging lenders to develop new ‘green’ mortgage products, to promote ownership of more efficient homes. In addition, lenders may need to start disclosing the energy performance of their entire mortgage book!

")

TALK TO AN EXPERT

Green mortgages are very much in their infancy, there’s only a few lenders offering them, and not a lot of competition.

Respect Mortgages works with an award winning mortgage broker who can help borrowers wherever they are in the UK (and even abroad).

Why not have a chat with one of their specialist advisers. They can explain what’s available and find you a mortgage from over 100 lenders that they deal with.